The HVAC industry has quietly transformed over the past decade. Global giants like Daikin, Carrier, Trane, and Gree have reshuffled their rankings, expanded into smart technologies, and adapted to market turbulence, all while chasing dominance in a $100+ billion global market.

Below, we’ve visualized key milestones from 2016 to 2024 showing how the top players evolved, merged, or fell behind. It’s a story of shifting power, bold bets, and industry disruption, and it sets the stage for where the HVAC world is headed next.

Key Takeaways

|

The Numbers That Define Our Industry

The global heating and cooling market presents a compelling growth story.

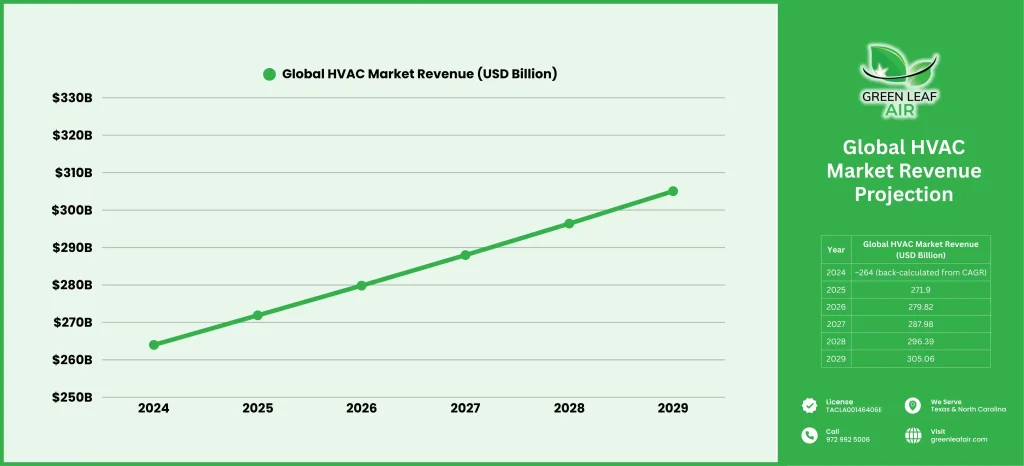

With worldwide revenue projected to reach $271.90 billion in 2025 and an expected compound annual growth rate (CAGR) of 2.91% through 2029, our industry continues to demonstrate resilience and expansion potential.

The United States remains the dominant market, expected to generate $129.63 billion in revenue by 2025, representing nearly half of the global market share.

What’s particularly striking is the per capita revenue figure of $34.80 in 2025, indicating the essential nature of HVAC systems in modern infrastructure and the industry’s ability to maintain steady demand even during economic uncertainties.

Market Leadership: The Big Players Define the Landscape

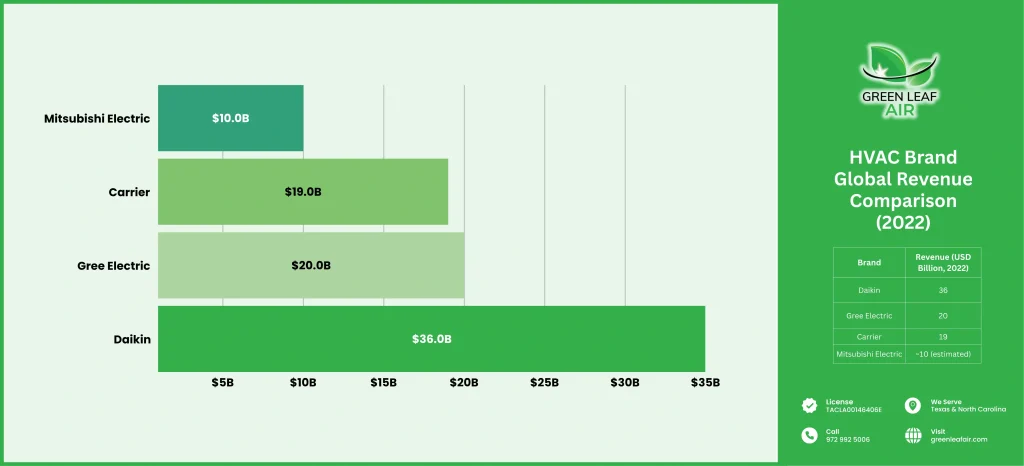

Daikin Industries: The Global Revenue Champion

The 2022 data reveals Daikin Industries of Japan as the undisputed global leader in steam and air conditioning supply, generating over $36 billion in revenue, positioning Daikin significantly ahead of its nearest competitors and underscoring the company’s successful global expansion strategy.

From a contractor’s perspective, Daikin’s market dominance reflects their strong product reliability, comprehensive distribution networks, and innovative technology integration.

Carrier: The North American Powerhouse

Carrier’s position in the market tells a compelling story of consistent leadership.

The 2016 data showed United Technologies Corporation’s Carrier segment holding one of the largest shares of the North American HVAC market, with UTC’s overall net sales reaching $66.5 billion in 2018.

By 2022, Carrier maintained its leadership position as the largest plumbing, heat, and air conditioning installation firm globally, with revenue exceeding $19 billion.

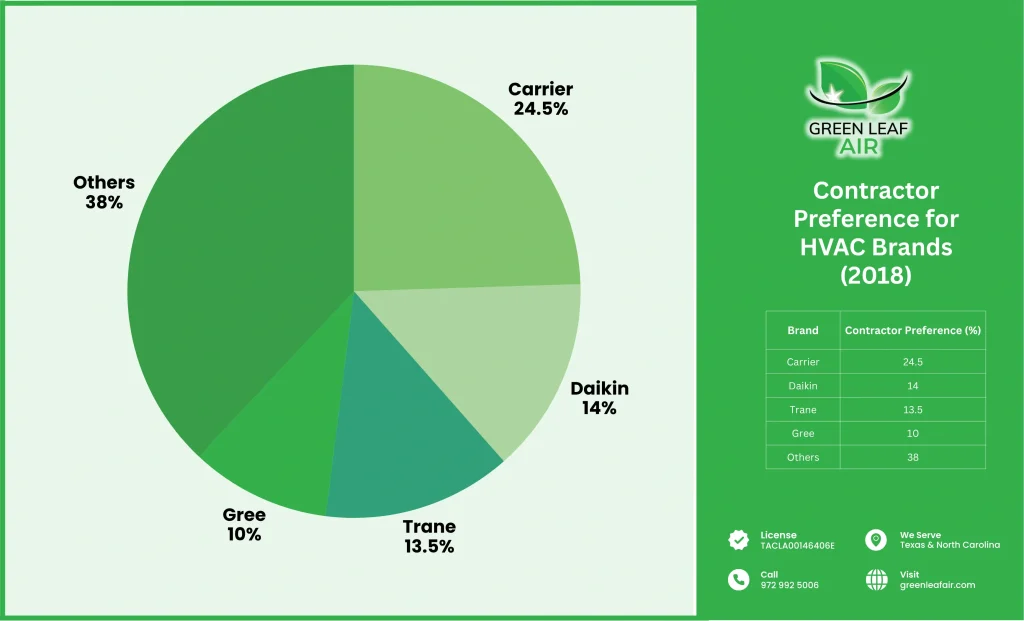

The 2018 brand preference data among U.S. construction firms is particularly revealing: 24.5% of respondents identified Carrier as their most-used HVAC brand.

This contractor preference translates directly into market share and demonstrates Carrier’s success in building strong relationships within the professional installation community.

The Asian Manufacturing Giants

Gree Electric Appliances from China emerged as another major player by 2022, generating over $20 billion in revenue alongside Carrier Global.

This represents the growing influence of Asian manufacturers in the global HVAC market, driven by competitive pricing, manufacturing efficiency, and increasing quality standards.

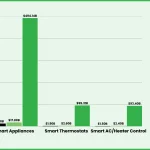

Mitsubishi Electric Corporation’s air conditioning and home products segment showed steady revenue growth from 2022 to 2024, with forecasts estimating 1.45 billion Japanese yen in revenue for 2025.

While smaller in absolute terms compared to the industry giants, Mitsubishi’s consistent growth trajectory indicates strong market positioning, particularly in the premium residential and light commercial segments.

Regional Market Dynamics: Understanding Geographic Concentration

North American Market Characteristics

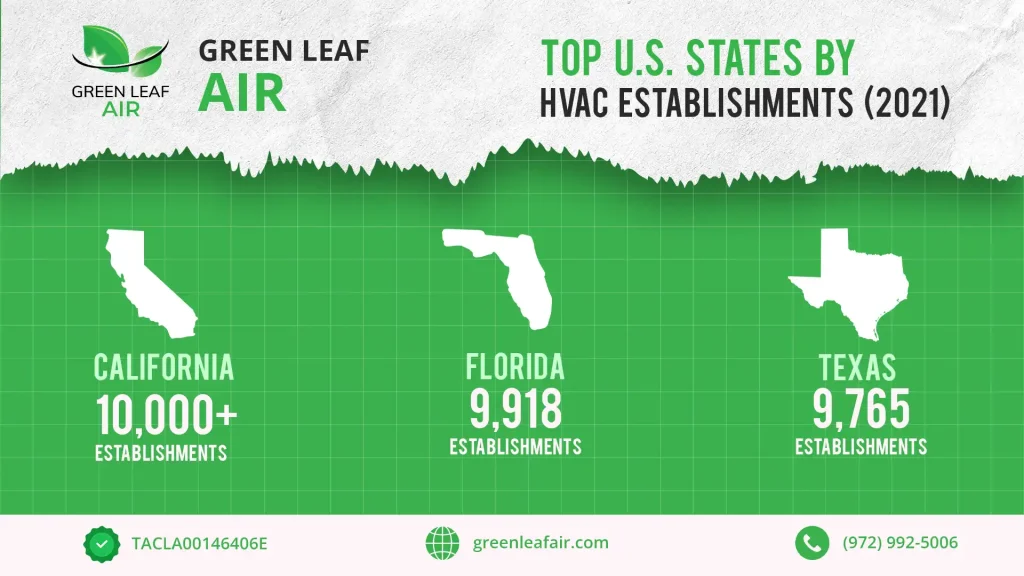

The 2021 data on HVAC company distribution across U.S. states reveals important regional dynamics.

California leads with the highest number of HVAC-related establishments, followed by Florida (9,918 establishments) and Texas (9,765 establishments).

This geographic concentration aligns with population density, climate demands, and construction activity levels.

Interestingly, the data shows that most establishments are plumbing, heating, and air-conditioning contractors rather than manufacturers or wholesalers.

This distribution pattern reflects the service-intensive nature of our industry and the critical role of local contractors in the value chain.

The Canadian and European Context

Ontario dominates the Canadian HVAC landscape, with British Columbia, Quebec, and Alberta following in establishment count.

This concentration pattern mirrors the U.S. market, where climate demands and economic activity drive HVAC business density.

The European market presents a different dynamic, with heat pump sales surpassing three million units in 2023.

This growth is driven by government policies promoting energy transition and environmental sustainability, creating opportunities for manufacturers specializing in heat pump technology.

Market Segmentation: Residential vs. Commercial Dynamics

The fundamental distinction between residential and commercial HVAC markets continues to shape competitive strategies.

The residential market’s relative simplicity, with fewer supply chain competitors and more consolidated manufacturing and distribution processes, creates different competitive dynamics compared to the commercial sector.

Commercial markets demand higher efficiency standards and involve more complex decision-making processes with multiple stakeholders.

This complexity creates opportunities for brands that can provide comprehensive solutions, technical support, and long-term service relationships.

Industry Foundation: Understanding HVAC Technology Integration

The heating, ventilation, and air conditioning (HVAC) industry is fundamentally based on technology used to provide thermal comfort and improve indoor air quality.

Generally, installation and controls are integrated into HVAC systems in individual buildings, however, HVAC systems may also be part of larger district heating/cooling networks.

The industry encompasses heating, ventilation, air conditioning, with the refrigeration segment often added to it, responsible for climate control and air quality in residential and commercial buildings.

This comprehensive scope provides information on the heating and cooling market, revenue of selected HVAC companies, and sales and demand data on heat pumps and air-conditioners.

Performance Trends: Reading Between the Lines

The AC Market Correction and Recovery

The North American air conditioner market experienced notable volatility, with shipments declining in 2022 and 2023 before beginning recovery in 2024.

This pattern reflects broader economic uncertainties, supply chain challenges, and changing consumer spending patterns.

For contractors, these fluctuations translate into inventory management challenges and the need for flexible business strategies.

North America was one of the regions with the highest demand for air conditioners, only behind Asia, where China and Japan had a really large market share.

Although the number of shipments for air conditioners in the U.S. had been stable until 2021, AC shipments fell noticeably in 2022 and 2023.

The Heat Pump Revolution

European heat pump sales growth represents one of the most significant trends in our industry.

Government incentives and environmental regulations are driving adoption rates that create substantial opportunities for manufacturers and installers specializing in this technology.

Heat pumps are considered an important technology for the energy transition, and some governments across Europe have been promoting them through public policy.

Global Competitive Landscape: International Brand Performance

Market Leadership Distribution

The first five companies in the global ranking were based in the U.S., with Nibe Industrier from Sweden being the first company from another country.

This demonstrates the continued strength of American HVAC manufacturers in global markets while also highlighting the emergence of strong European competitors.

Technology and Efficiency Trends

In the United States, the trend in the heating and cooling market shows growing demand for energy-efficient and eco-friendly HVAC systems.

This shift toward sustainability creates opportunities for manufacturers investing in advanced technologies and challenges those relying on traditional, less efficient solutions.

Competitive Analysis: Brand Positioning and Strategy

Carrier’s Sustained Leadership Strategy

Carrier’s consistent market leadership from 2016 through 2022 demonstrates the value of brand recognition, distribution network strength, and product reliability.

Their 24.5% contractor preference rate in 2018 reflects successful relationship building with the professional installation community.

Daikin’s Global Expansion Success

Daikin’s achievement as the global revenue leader by 2022 represents successful international expansion and product portfolio diversification. Their strategy appears focused on technology innovation and market presence in key regions.

The Rise of Chinese Manufacturers

Gree Electric Appliances’ emergence as a $20+ billion revenue company represents the growing competitiveness of Chinese manufacturers in global HVAC markets.

This trend challenges traditional market leaders and creates pricing pressures throughout the industry.

Mitsubishi’s Steady Growth Strategy

Mitsubishi Electric Corporation’s air conditioning and home products segment includes home products, air conditioners, electronic appliances, fans, televisions, and fridges, showing diversification beyond a pure HVAC focus.

Between 2022 and 2024, the revenue of this segment increased steadily, demonstrating consistent market performance.

Industry Forecasts: Looking Toward 2029

Market Growth Projections

The projected 2.91% CAGR through 2029 suggests steady, sustainable growth rather than explosive expansion.

This growth rate indicates market maturity while still providing opportunities for companies that can effectively compete on technology, service, and efficiency.

Geographic Growth Opportunities

With the U.S. maintaining its position as the largest market ($129.63 billion projected for 2025), opportunities exist for both domestic and international brands to expand their American market presence.

However, the data suggests that success requires significant investment in distribution networks and contractor relationships.

Technology-Driven Differentiation

The heat pump growth in Europe and the energy efficiency focus in the U.S. indicate that technology innovation will be crucial for maintaining a competitive advantage.

Brands that invest in heat pump technology, smart systems, and energy efficiency improvements are likely to outperform those maintaining traditional product lines.

Strategic Implications for Industry Professionals

For Contractors and Installers

Brand selection should consider not just initial cost but also contractor support, training programs, warranty coverage, and customer satisfaction rates.

Carrier’s 24.5% contractor preference rate suggests that professional support and reliability remain crucial decision factors.

For Distributors

The concentration of establishments in key states (California, Florida, Texas) indicates where distribution investments will likely generate the highest returns.

Understanding regional preferences and climate-specific requirements becomes essential for inventory and sales strategies.

For Manufacturers

The data suggests that global leadership requires either massive scale (like Daikin’s $36 billion revenue) or strong regional positioning (like Carrier’s North American dominance).

Mid-sized manufacturers may find success through specialization in specific technologies or market segments.

Risk Factors and Market Challenges

Supply Chain Vulnerabilities

The AC shipment declines in 2022-2023 demonstrate the industry’s vulnerability to supply chain disruptions and economic uncertainties.

Companies with diversified supply sources and flexible manufacturing capabilities appear better positioned to navigate these challenges.

Competitive Pressure from Asian Manufacturers

The success of companies like Daikin and Gree Electric Appliances indicates increasing competitive pressure from Asian manufacturers.

Traditional Western brands must focus on technology innovation, service quality, and brand differentiation to maintain their market position.

Regulatory and Environmental Pressures

European heat pump growth driven by government policies suggests that regulatory changes will continue to influence market dynamics.

Companies must adapt their product portfolios to meet evolving environmental standards and efficiency requirements.

Market Structure and Business Model Insights

UTC’s Integrated Business Model

UTC Climate, Controls & Security is owned by UTC and provides HVAC products as well as fire safety and security solutions.

This integrated approach demonstrates how major players leverage synergies across related building systems and technologies.

Industry Consolidation Patterns

The residential market tends to be less complex than the commercial sector due to fewer competitors along the supply chain and the consolidation of the manufacturing and distribution processes.

This suggests ongoing consolidation opportunities in residential-focused segments.

Conclusion

From 2016 to 2024, the HVAC industry has shown steady growth amid evolving technology and increasing global competition.

Carrier leads in North America, Daikin dominates globally, and Chinese brands like Gree are emerging strong, highlighting a market where innovation and reliability matter most.

By 2029, the global HVAC market is projected to reach $271.9 billion with 2.9% annual growth, driven by energy efficiency, heat pump adoption, and smart system integration.

Success will depend on adapting to these trends, supporting professional partners with training and resources, and understanding regional market needs.

As competition grows more complex, HVAC companies must combine strategic vision, technology adaptation, and local insight to thrive.

FAQs

How Do Contractors Choose Between Brands Like Carrier, Daikin, And Gree?

Contractors prioritize reliability, technical support, warranty, and local distributor relationships over price. Carrier’s strong contractor preference reflects its focus on training, support, and distribution networks.

Why Is Daikin A Global Leader Despite A Lower U.S. Presence?

Daikin’s growth comes from strategic expansion in Asia and Europe, where energy-efficient heat pumps and VRF systems meet strict regulations and customer demand.

Why Are Heat Pump Sales Booming In Europe But Are Slower In North America?

Europe’s growth is fueled by government incentives and carbon reduction policies. North America’s slower adoption reflects different regulations, natural gas infrastructure, and climate factors.

How Do California, Florida, And Texas Shape HVAC Brand Strategies?

These states have the largest contractor bases and installation volumes. Brands focus their support, training, and distribution here to build loyalty and national market strength.

What Metrics Help Predict Future HVAC Brand Market Share?

Key indicators include contractor preference surveys, regional growth, technology adoption, revenue trends, distribution expansion, policy changes, and manufacturer support programs.

Methodology

This analysis draws exclusively from eight Statista Research Department reports (2016–2024), with projections through 2029. It combines quantitative and qualitative data to examine key HVAC market trends globally.

- Data Source: All data sourced from Statista Research Department publications.

- Time Frame: Covers data from 2016–2024, with projections to 2029.

- Revenue Analysis: Evaluated in constant dollars; growth projected using CAGR.

- Market Scope:

- Global, North American, and European HVAC markets

- Segmented into residential and commercial sectors

- Key Metrics Analyzed:

- Brand performance and contractor preferences

- Market share and geographic concentration

- Competitive positioning using both quantitative metrics and qualitative insights

- Regional Insights: Includes state-level establishment data and international revenue comparisons to identify market leaders and emerging regions.